House costs have held up higher than anticipated amid excessive rates of interest. However that doesn’t imply the housing market is wholesome.

When the Federal Reserve started elevating rates of interest in 2022, most economists thought the housing market could be the primary to endure the implications: Increased borrowing prices would make it costlier to purchase and to construct, resulting in decreased demand, much less development and decrease costs.

They had been proper — at first. Building slowed, however then picked up. Costs hiccuped, then resumed their upward march. Increased charges made properties tougher to afford, however Individuals nonetheless needed to purchase them.

The result’s a housing market that’s totally different, and stranger, than the one described in economics textbooks. Elements have proved surprisingly resilient. Different components have seized up virtually fully. And a few appear perched on a precipice, vulnerable to tumbling if charges keep excessive too lengthy or the financial system weakens unexpectedly.

Additionally it is a market of stark divides. Individuals who locked in low charges earlier than 2022 have, typically, had their house values soar however have been insulated from larger borrowing prices. Those that didn’t already personal, then again, have usually had to decide on between unaffordable rents and unaffordable house costs.

However the scenario is nuanced. Owners in some components of the nation face skyrocketing insurance coverage prices. Rents in some cities have moderated. Builders are discovering methods to make new properties reasonably priced for first-time consumers.

Nobody indicator tells the total story. Fairly, economists and business specialists say understanding the housing market requires an array of information shedding mild on totally different items of the puzzle.

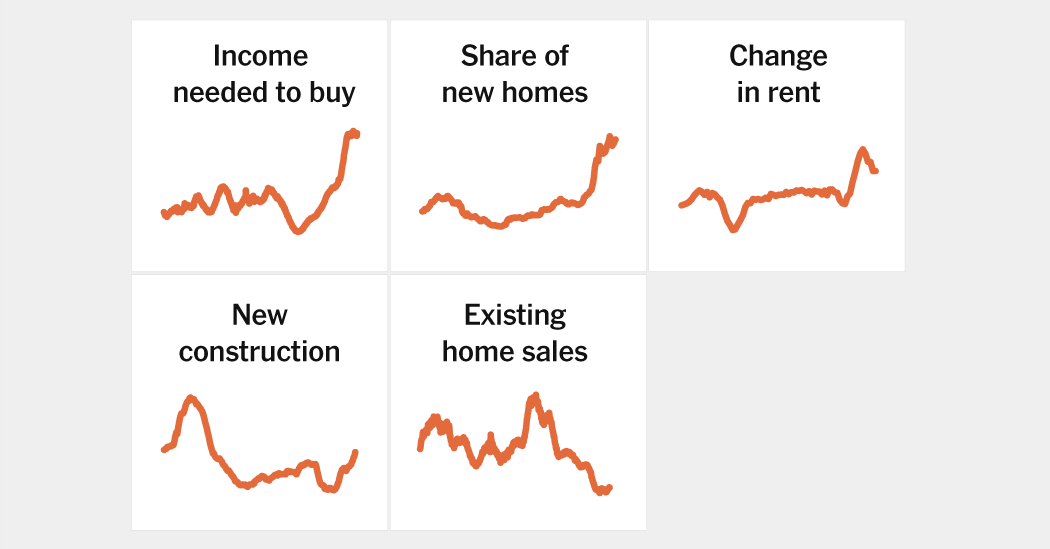

1. It’s laborious to discover a house to purchase.

The fast rise in rates of interest pushed down demand for housing, by making it costlier to borrow. However it additionally led to a giant drop in provide: Many house owners are holding onto their properties longer than they might in any other case as a result of promoting would imply giving up their ultralow rates of interest.

This “price lock” phenomenon has contributed to a extreme scarcity of properties on the market. It isn’t the one issue: House constructing lagged for years earlier than the pandemic, and retired child boomers have been selecting to remain of their properties quite than transferring to retirement communities or downsizing to condominiums as many housing specialists had anticipated.

Many economists argue that the shortage of provide has helped preserve costs excessive, notably in some markets, though they disagree in regards to the magnitude of the impact. What is definite is that for anybody hoping to purchase, discovering a house has been extraordinarily tough.

2. Properties are unaffordable.

House costs, already excessive, soared through the pandemic, rising greater than 40 % nationally from the top of 2019 to mid-2021, in accordance with the S&P CoreLogic Case-Shiller worth index. They’ve risen extra slowly since then, however they haven’t fallen as many economists anticipated when the Fed began elevating rates of interest.

Rising rates of interest have put these costs even additional out of attain for a lot of consumers. Somebody shopping for a $300,000 home with a ten % down fee may count on to pay about $1,100 a month on a mortgage in late 2021, when rates of interest on a 30-year, fixed-rate mortgage had been about 3 %. As we speak, with charges at about 7 %, that very same home would price about $1,800 a month, a rise of about 60 % in month-to-month prices. (That doesn’t even have in mind the rising price of insurance coverage or different bills.)

Economists have other ways of measuring affordability, however all of them present just about the identical factor: Shopping for a home, notably for first-time consumers, is additional out of attain than at any level in many years, or possibly ever. One index, from Zillow, reveals that the standard family shopping for the median house with 10 % down may count on to spend greater than 40 % of their revenue on housing prices, properly above the 30 % that monetary specialists suggest. And in lots of cities, resembling Denver, Austin and Nashville — by no means thoughts longtime outliers like New York and San Francisco — the numbers are a lot worse.

3. New properties are filling (a few of) the hole.

Maybe probably the most stunning improvement within the housing market over the previous two years has been the resilience of new-home gross sales.

Builders usually battle when rates of interest rise, as a result of excessive borrowing prices drive away consumers whereas additionally making it costlier to construct.

However this time round, with so few present properties accessible on the market, many consumers have been turning to new development. On the identical time, many massive builders had been capable of borrow when rates of interest had been low, and have been ready to make use of that monetary firepower to “purchase down” rates of interest for purchasers — making their properties extra reasonably priced while not having to chop costs.

Consequently, gross sales of recent properties have held comparatively regular at the same time as gross sales of present properties have plummeted. Builders have particularly sought to cater to first-time consumers by constructing smaller properties, a section of the market all of them however ignored for years.

It isn’t clear how lengthy the pattern can proceed, nevertheless. Many builders pulled again on exercise when charges first rose, leaving fewer new properties within the pipeline to come back to market within the years forward. And if charges keep excessive, it could get tougher for builders to supply the monetary incentives they’ve used to draw first-time consumers. Non-public builders in Could broke floor on new properties on the slowest price in practically 4 years, the Commerce Division mentioned on Thursday.

4. Rents are unaffordable, too.

Rents skyrocketed in a lot of the nation through the pandemic, as Individuals fled cities and sought area. Then they saved rising, because the robust labor market elevated demand.

Rising rents helped gasoline an apartment-building increase, which has introduced a flood of provide to the market, notably in Southern cities like Austin and Atlanta. That has led rents to rise extra slowly and even to fall in some locations.

However that moderation has been sluggish to work its means via the market. Many tenants are paying rents negotiated earlier within the housing cycle, and the brand new development has been concentrated within the luxurious market, which doesn’t do a lot to assist middle- or lower-income renters, no less than within the brief time period.

All of that has produced a rental affordability disaster that retains rising worse. A record share of renters are spending greater than 30 % of their revenue on housing, Harvard’s Joint Middle for Housing Research discovered lately, and greater than 12 million households are spending greater than half their revenue on hire. Affordability is now not only a downside for the poor: The Harvard report discovered that hire is turning into a burden even amongst many households incomes greater than $75,000 a 12 months.

5. A shift could also be underway.

For a lot of the previous two years, the housing market — particularly for present properties — has been caught. Consumers can’t afford properties except both costs or rates of interest fall. House owners really feel little strain to promote, and aren’t desirous to turn out to be consumers.

What may break the logjam? One chance is decrease rates of interest, which may convey a flood of each consumers and sellers again to the market. However with inflation proving cussed, price cuts don’t seem imminent.

One other chance is a extra gradual return to regular, as homeowners resolve they will now not delay long-delayed strikes and turn out to be extra keen to chop a deal, and as consumers resign themselves to larger charges.

There are indicators which may be starting to occur. Extra homeowners are itemizing their properties on the market, and extra are reducing costs to draw consumers. Builders are ending extra new properties with out a purchaser lined up. Actual property brokers are sharing anecdotes of empty open homes and houses that sit in the marketplace longer than anticipated.

Hardly anybody expects costs to break down. The millennial technology is within the coronary heart of the home-buying years, that means demand for properties must be robust, and years of under-building imply the nation nonetheless has too few properties by most measures. And since most householders have loads of fairness, and lending requirements have been tight, there isn’t prone to be a wave of compelled gross sales as there was when the housing bubble burst practically twenty years in the past.

However that additionally implies that the affordability disaster isn’t prone to resolve itself quickly. Decrease charges would assist, however it would take greater than that for homeownership to really feel achievable to many youthful Individuals.